The Australian soil carbon market is booming, but the tax and accounting rules are anything but straightforward. Division 420, rolling balance methods, primary producer concessions that only apply to some entities, GST-free treatment with hidden traps, and aggregator arrangements that can undo your tax benefits entirely.

National Accounts works with farmers, landholders, carbon project developers and aggregators across Australia to navigate the full lifecycle of soil carbon credits.

1 How soil carbon credits work under the ACCU Scheme

Australian Carbon Credit Units (ACCUs) are issued by the Clean Energy Regulator under the Carbon Credits (Carbon Farming Initiative) Act 2011. Each ACCU represents one tonne of CO2 equivalent stored or avoided. For soil carbon, the dominant pathway is the 2021 Soil Carbon Method covering grazing, cropping, and mixed farming systems.

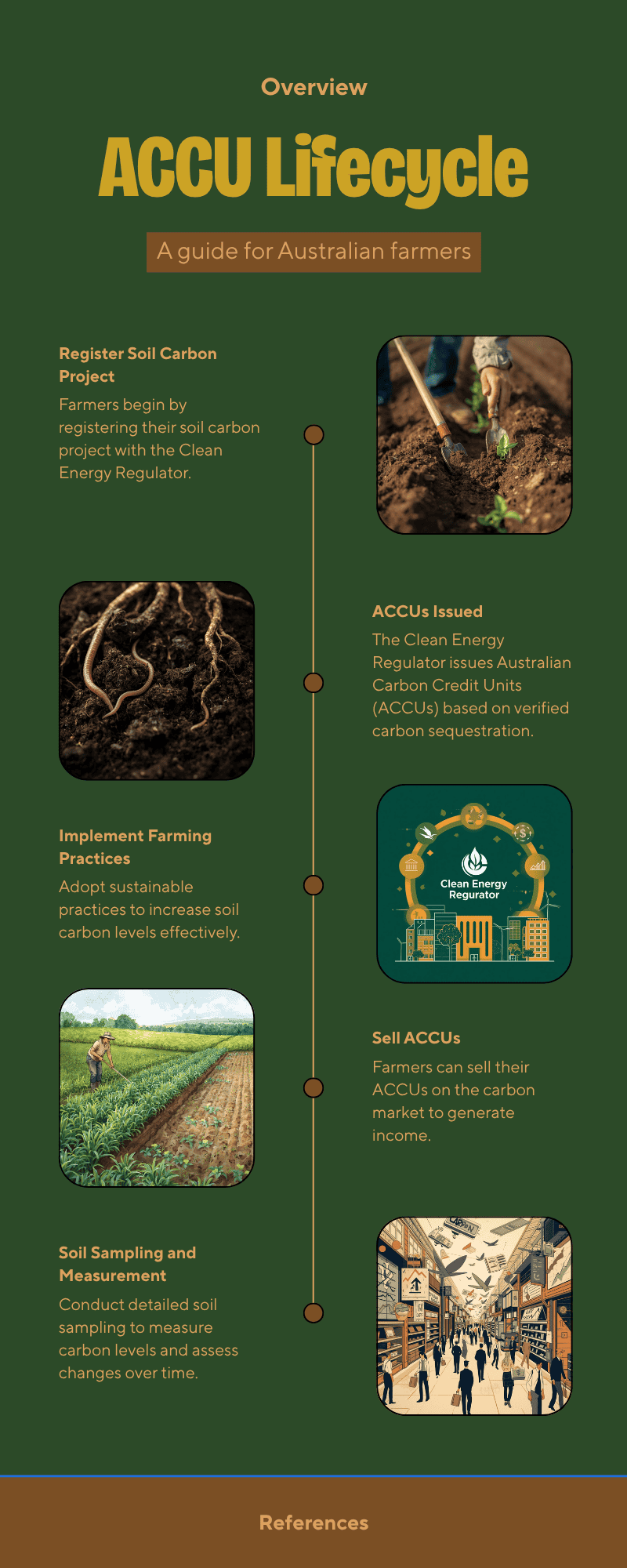

Register a Project

Apply to the Clean Energy Regulator under an approved methodology. Projects commit to 25-year or 100-year permanence periods.

Measure & Monitor

Baseline soil sampling establishes starting carbon levels. Ongoing measurement verifies sequestration through changed farming practices.

ACCUs Issued

The Clean Energy Regulator issues ACCUs based on verified carbon sequestration. Credits are held in the Australian National Registry.

Sell or Surrender

Sell ACCUs on the open market (~$36/unit), through a Carbon Abatement Contract, or to Safeguard Mechanism entities needing offsets.

Tax & Accounting

Division 420 applies a rolling balance method, primary producer concessions change the rules, and GST treatment varies by credit type.

Aggregator Structures

Whether a Carbon Service Provider arrangement is a lease or service contract critically affects your tax treatment.

2 Tax treatment of soil carbon credits

Division 420: the rolling balance method

ACCUs are classified as registered emissions units (REUs) and taxed exclusively under Division 420 of the ITAA 1997. Normal CGT rules do not apply. Instead, a rolling balance method operates where the cost of acquisition is deductible when the unit is first held, and year-end value changes are either included in assessable income (if value increases) or claimed as a deduction (if value decreases).

Taxpayers choose from three valuation methods: FIFO cost (default), actual cost, or market value, and cannot change methods within four years. For ACCUs issued by the Clean Energy Regulator, the cost base is market value immediately after the holder begins to hold them.

Proceeds from disposal are assessable income deemed to have an Australian source. Carbon credit income is taxed on revenue account. The CGT discount does not apply.

GST treatment: ACCUs are GST-free

Under Subdivision 38-S of the GST Act, supplies of eligible emissions units including ACCUs are GST-free. No GST is charged on ACCU sales, but input tax credits can still be claimed on related acquisitions (soil testing, consultant fees, monitoring costs).

Watch out for international credits: Non-registered carbon units (Verra VCUs, Gold Standard VERs) are not covered by the GST-free exemption and generally attract GST unless supplied to entities outside Australia.

| Legislation | What it covers |

|---|---|

| ITAA 1997, Division 420 | Core income tax rules for all registered emissions units (rolling balance method) |

| ITAA 1997, Subdivision 420-BA | Primary producer concessional ACCU treatment (from 1 July 2022) |

| GST Act, Subdivision 38-S | GST-free treatment of eligible emissions units |

| ITAA 1997, Subdivision 40-J | Carbon sink forest establishment deductions |

| Carbon Credits (CFI) Act 2011 | ACCU Scheme establishment, project eligibility, methodology determinations |

| Safeguard Mechanism (Crediting) Amendment Act 2023 | Reformed baselines, introduced Safeguard Mechanism Credits (SMCs) |

3 Primary producer concessions that change everything

The Treasury Laws Amendment (2023 Measures No. 2) Bill 2023 introduced three transformative concessions for eligible individual primary producers holding “Primary Producer Registered Emissions Units” (PPREUs). These changes were retrospective to 1 July 2022.

Tax deferred to sale

Eligible farmers are not taxed on annual rolling-balance value changes. This eliminates the “phantom income” problem where unsold ACCUs generate tax liabilities with no cash to pay them.

FMD eligible income

ACCU sale proceeds are treated as primary production income for Farm Management Deposit purposes. Critical because FMDs require non-primary-production income below $100,000.

Income averaging

ACCU sale proceeds qualify for income tax averaging, smoothing the tax impact of lumpy carbon credit sales across years, just like livestock or crop income.

4 Accounting for carbon credits in financial statements

There is no specific AASB or IFRS standard addressing carbon credits. Entities must develop accounting policies under the AASB 108/IAS 8 hierarchy.

Two permissible classifications

- Inventory (AASB 102): Appropriate when ACCUs are held for sale in the ordinary course of business. Measured at lower of cost and net realisable value.

- Intangible asset (AASB 138): Appropriate when held for investment or to surrender against Safeguard Mechanism compliance obligations.

ACCUs are not financial instruments. Despite being tradeable under the Corporations Act, ACCUs do not meet the AASB 132 definition. AASB 9/IFRS 9 does not apply.

Key accounting considerations

- Initial measurement: Generated ACCUs are treated as government grants under AASB 120/IAS 20, with a choice of fair value or nominal initial measurement.

- Revenue recognition: ACCU sales follow the AASB 15/IFRS 15 five-step model. Timing depends on when control transfers.

- Aggregator arrangements: The principal versus agent determination under AASB 15 is critical. Pooling arrangements may risk classification as a Managed Investment Scheme.

5 How National Accounts helps carbon farming clients

We work with clients across every stage of the carbon credit lifecycle.

Entity Structuring

Analyse whether your farming structure maximises access to primary producer concessions before you register a carbon project.

Division 420 Compliance

Annual rolling balance calculations, valuation method selection, and correct tax return reporting for ACCU holdings.

Primary Producer Concessions

Verify eligibility, assess connected-area requirements, and ensure your arrangement preserves concessional treatment.

FMD & Income Averaging

Integrate carbon credit income with Farm Management Deposits and averaging to smooth tax outcomes across variable years.

GST & BAS Compliance

Correct GST treatment of ACCU sales, input tax credit claims on project costs, and accurate BAS reporting.

Financial Statements

Classify and measure ACCUs correctly under AASB standards with appropriate disclosures.

Aggregator Advisory

Review CSP agreements for tax implications. Assess principal vs agent classification, AFSL exposure, and MIS risk.

Sale Timing Strategy

Plan ACCU sale timing and volume to optimise tax, manage PAYG instalments, and coordinate with other farm income.

6 Frequently asked questions

How are soil carbon credits taxed in Australia?

Are carbon credits GST-free in Australia?

What are the primary producer carbon credit concessions?

Can I use carbon credit income with Farm Management Deposits?

How should carbon credits appear in my financial statements?

Do trusts and companies get the same concessions as individual farmers?

What tax deductions can I claim for carbon farming costs?

Does my aggregator arrangement affect my tax treatment?

Ready to get your carbon credits sorted?

Book a free consultation. We will review your situation and give you a clear roadmap for tax, compliance, and maximising your concessions.

Book Your Free Consultation